Direct selling origins trace back deep into human history. It all started from peddlers who sold their goods to nearby towns and even to homesteads back in the 1700s. Fast forward to the 21st century, direct sales now empower individuals worldwide to become entrepreneurs and generate income. What began as a simple, personal way of doing business has now become a global phenomenon adapting with each new era.

The road to global growth is ongoing. Even with everything that’s happened—political issues, economic challenges, and the pandemic, the industry has really shown how resilient it can be,

Global retail sales of the direct selling market have grown by 1% over the past 4 years.

Source: WFDSA

This is where Epixel’s research team went all in on the World Federation of Direct Selling Associations’ (WFDSA) latest finding, and the analysis took off. Our complete study set sail to reveal intricate details of the direct selling industry, examining its global distribution, economic impact, GDP levels and market size. We’ve also touched upon how different regions embrace direct selling, from mature markets in North America and Europe to the up-and-coming sectors in Asia-Pacific and Latin America. The later part delves deeper into key factors that are shaping the direct selling industry as whole.

It’s about getting a real sense of what makes each market tick and where the next big opportunities lie.

Understanding the direct selling penetration into global markets

In this section, we take a closer look at how direct selling has made its way into almost every country and region around the world. Its growth across various economies, GPD levels and market size is analyzed and discussed to show how well the direct selling industry can fit into different settings.

How direct selling penetrates different countries

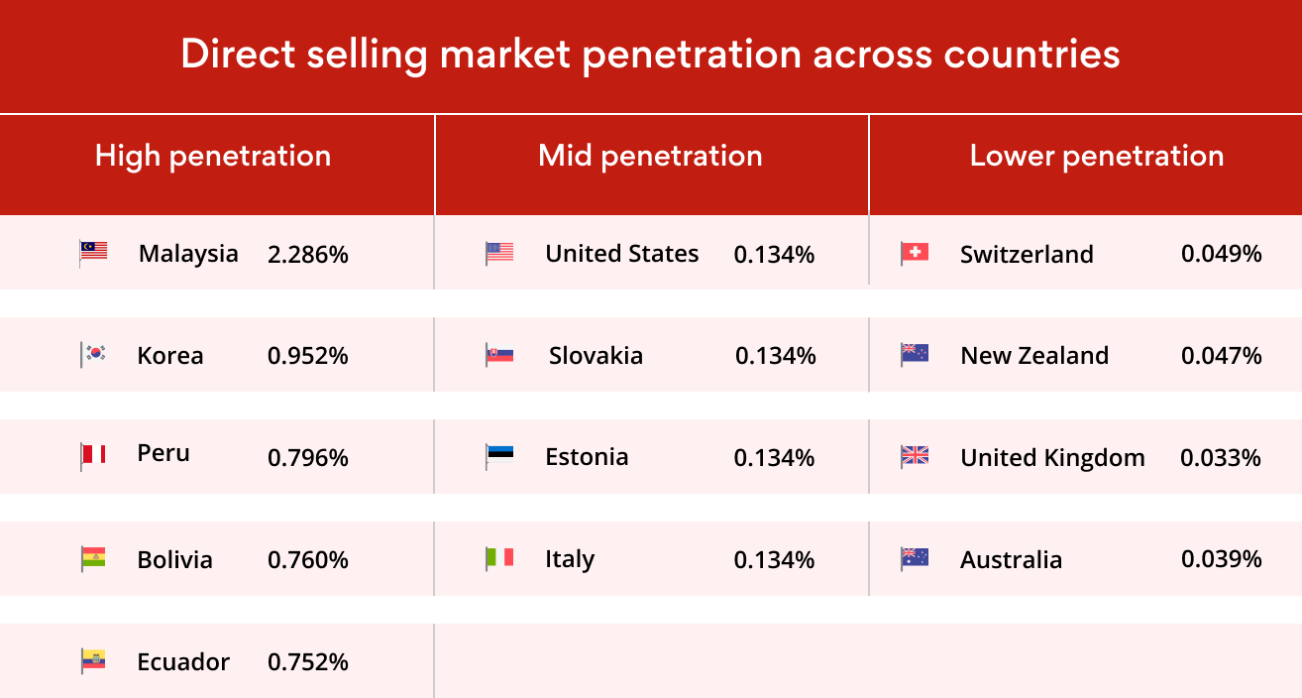

WFDSA analyzed market penetration for direct selling across 63 countries. The metric involved first dividing each country's direct sales by its GDP and then expressing the result as a percentage. The results were then ranked from highest to lowest and categorized into three groups:

1. High penetration markets are those where direct selling has deeply embedded itself in the economy. Five markets lead the pack,

- Malaysia (2.286%)

- Korea (0.952%)

- Peru (0.796%)

- Bolivia (0.760%)

- Ecuador (0.752%)

These countries top the list in direct sales as a percentage of their GDP, which points to mature and potentially lucrative markets.

2. Mid penetration markets indicate a developing interest and engagement within the direct selling industry and signal a positive trend in acceptance. The countries comprise of:

- United States (0.134%)

- Slovakia (0.134%)

- Estonia (0.134%)

- Italy (0.131%)

These markets portray the potential for growth and deeper integration of direct selling as they continue to evolve and attract more participants.

3. Lower penetration markets reflect a modest presence of the industry within the economy. Few include:

- Switzerland (0.049%)

- New Zealand (0.047%)

- United Kingdom (0.033%)

- Australia (0.039%)

While there’s great potential for expansion in these regions, challenges like market saturation and consumer preferences could pose difficulties for growth.

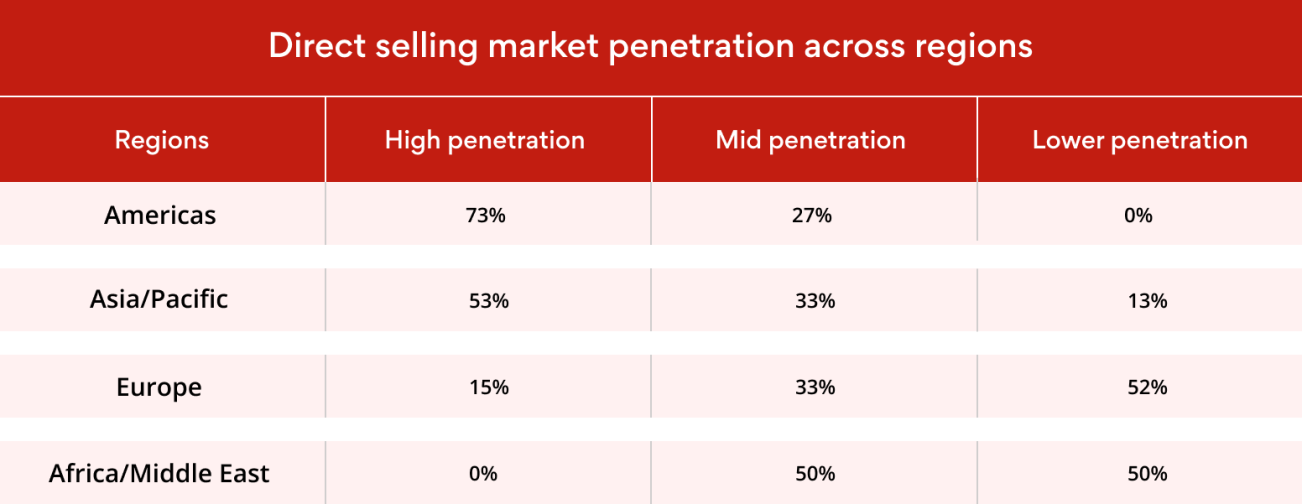

How direct selling penetrates various regions

The way direct selling penetration varies by region is highly fascinating. While some regions have adopted direct selling up to great levels, others are still finding their place in the market, revealing potential. Cultural attitudes, economic conditions, and the maturity of the market all play a part in these variations. Using this knowledge about regional characteristics, MLM businesses can adjust their strategies to navigate new markets and address challenges unique to each region better.

1. Americas

- High penetration: A notable 73% of countries in the Americas exhibit strong direct selling presence, fostering active networks of independent agents and entrepreneurial opportunities.

- Mid penetration:A smaller portion, 27% of countries show moderate interest. This indicates a potential for growth in the years to come.

- Lower penetration: Interestingly, no countries are categorized as having low penetration, which signifies that all markets have embraced the robust nature of direct selling throughout the region.

2. Asia/Pacific

- High penetration: Over half the region, 53%, is highly engaged in direct selling with well-developed networks.

- Mid penetration: Around 33% of the countries show moderate engagement, indicating potential for expansion with some market challenges still in play.

- Lower penetration: Though a smaller segment (13%), the region represents opportunities for companies to introduce and expand direct selling operations.

3. Europe

- High penetration: Only a small portion, 15% of European countries have a strong foothold in direct selling.

- Mid penetration: A third of the region, 33%, sees moderate direct selling activity, with potential for further development and growth.

- Lower penetration: 52% of European countries fall into this category, facing challenges in embracing direct selling completely. It suggests potential challenges or saturation in this market.

4. Africa/Middle East

- High penetration: No countries in this market are categorized under high penetration. This may point out that direct selling is still an emerging opportunity with high growth potential in this market.

- Mid penetration: Half of the countries (50%) meet with mid-penetration levels. There’s a steady interest in direct selling with room for growth and further market engagement.

- Lower penetration: The other half of the countries have low penetration, which shows that direct selling markets are still in their early stages or have not fully developed in these areas.

How economic classification influences direct selling penetration

The economic impact on direct selling can’t be overstated as it determines how businesses can thrive in this space. It influences everything from revenue and production to the entrepreneurial energy of individuals. In developing economies, direct selling often flourishes because people seek flexible income opportunities. On the flip side, there are advanced economies which might hold back direct selling growth due to challenges like consumers sticking to established retail options or changing behaviors. In detail with supporting data:

1. Developing economies

- High penetration: More than half, 53% of developing countries fall into this category, showcasing a strong acceptance of direct selling as a business model. This high penetration can be attributed to several factors like a rising number of individuals turning to direct selling as a means to grow and generate income.

- Mid penetration: 37% of developing countries exhibits mid-level penetration. This can be seen as a positive sign of economic development, as it often correlates with increasing consumer spending power and openness to new business opportunities.

- Lower penetration: Only 10% have low penetration. This suggests that direct selling is forming into a robust channel in developing markets.

2. Advanced economies

- High penetration: 15% of advanced economies achieve high penetration in direct selling. This percentage tells how challenges still continue to gain a foothold in these regions.

- Mid penetration: About 30% of advanced economies experience mid-level penetration. 30% fall into mid-penetration. These countries may have potential for growth in direct selling but not the same as seen in developing countries.

- Lower penetration: A notable resistance to direct selling can be seen with a significant 55% of advanced economies coming under this category. This highlights the difficulty for direct sales companies to penetrate these markets.

The top five countries in the National Entrepreneurship Context Index (NECI) measures the positiveness of a country's entrepreneurial environment. The countries include:

- United Arab Emirates

- India, Saudi Arabia

- Lithuania

- Qatar

Interestingly, only Lithuania, an advanced economy, makes to this list.

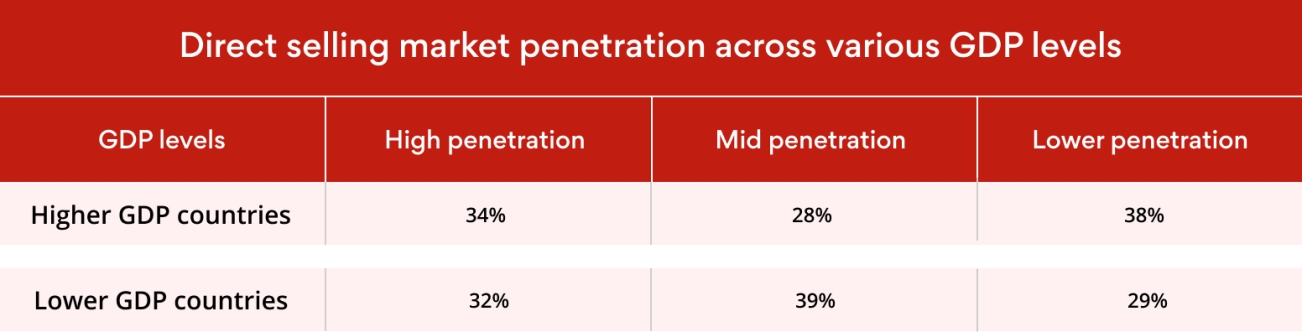

How different GDP levels shape direct selling market penetration

Market penetration within the direct selling sector and a nation's GDP levels tend to be very closely correlated. It's a very important indicator to assess whether the economy is healthy as a whole and whether consumers have sufficient spending power. For example, low-GDP markets opt for direct selling because entrepreneurship and income generation are needed, whereas high-GDP markets seek a niche-based, customer-centric approach.

Higher GDP countries

- High penetration: A notable percentage, 34% of higher GDP countries achieve high penetration in direct selling. It indicates a market in which the business has created a space to thrive even though the competition is fierce. This mainly encompasses niche markets, quality products, and a focus on wellness and sustainability.

- Mid penetration: Around 28% of these countries show a small level of direct selling penetration. It reflects a balance between changing customer behavior and the appeal of direct selling business to deliver personalized experiences.

- Lower penetration: A significant 38% of high-GDP countries exhibit low penetration in direct selling, which indicates a balanced distribution.

Lower GDP countries

- High penetration: Direct selling finds fertile ground in 32% of lower GDP countries. Here it serves as a key income source for individuals, leveraging the entrepreneurial drive and community-based networks which can be seen in these regions.

- Mid penetration: The largest share, 39%, falls into the mid-level penetration category. This suggests that many lower GDP countries are in a growth phase for direct selling.

- Lower penetration: 29% of lower GDP countries experience low penetration. It shows that a strong economy doesn’t necessarily hinder direct selling success.

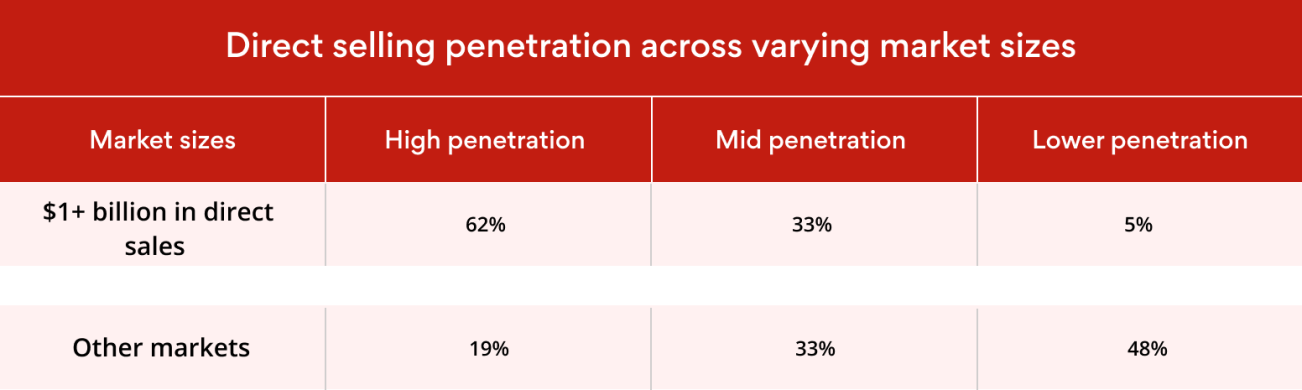

How variations in market size impact direct selling penetration strategies

Market size can have a direct influence on how deeply direct selling can penetrate a region. Larger markets offer greater potential for growth when compared to smaller markets. A basic idea of the dynamics of market size will surely help direct selling companies tailor their strategies in order to optimize their reach, far and wide.

Markets generating over $1 billion in annual direct sales

- High penetration: A substantial 62% of these large markets achieve high direct selling penetration, signaling the rate at which customers are familiar with this business model. The size of the market also supports diverse product offerings.

- Mid penetration: Around 33% of these markets exhibit mid-level penetration, which portrays a growing acceptance of direct selling.

- Lower penetration: With only 5% experiencing low penetration, it’s clear that robust direct selling revenues are tied to increased market penetration.

Other markets

- High penetration: In smaller or less established markets, only 19% achieve high penetration. Thus, giving way to more competition and more challenges.

- Mid penetration: 33% of these other markets show mid-level penetration and suggest a balanced interest in direct selling.

- Lower penetration: The fact that 48% have low penetration signifies the challenges associated with scaling direct selling in smaller markets.

Discover how we build resilient businesses with advanced MLM functionalities

Strategic implications for the direct selling industry

While looking ahead in direct selling, it's good to keep some strategic ideas in mind. These insights can help businesses, small or big, strengthen their operations and find new chances to grow. Here are some key points to consider:

1. Expanding into new markets: Identifying regions with lower direct selling penetration, especially in developed regions, helps in strategic expansion efforts. Tailoring strategies to suit local market dynamics remains the key.

2. Prioritizing high-penetration regions: Another key lies in knowing how to make the most of existing strong markets. Companies can tap into the existing infrastructures and consumer knowledge of direct selling models in these regions.

3. Growth opportunities in underpenetrated areas: There’s untapped potential in less saturated markets, Europe and Africa/Middle East, for instance. Still, strategies should factor in the potential for market saturation in Europe and the developmental issues in Africa and the Middle East.

4. Focusing on developing economies: The penetration level is relatively high in developing countries, at 53%, and thus holds great investment and growth prospects. Better success rates are when strategies are devised while being cognizant of the local economic factors as well as consumer behaviors.

5. Leveraging high GDP markets: The penetration of 34% in higher GDP countries hints at the fact that indeed these high-income markets are capable of sustaining direct selling activities. Coming up with strategies for balancing between high and lower GDP markets can help to reduce risks and attract diverse consumer segments.

6. Capitalizing on large market sizes: Prime targets seem to be countries that have high yearly sales, exceeding $1 billion. When a company has a solid foothold or is expanding its market share in these areas, it can greatly enhance its overall performance.

7. Addressing challenges in lower penetration markets: Critical to pre-entry in low-penetration regions and market areas lies a complete analysis of the barriers inherent within that environment. This may include regulatory barriers and cultural barriers or competitive landscapes. Then customized strategies have to be conceptualized to overcome them and facilitate successful growth.

Who are the driving forces behind global direct selling penetration?

The direct selling industry embraces and welcomes diversity. This diversity is the pulse that innovates global direct selling penetration to a whole new level. And so, we've done the legwork for you and covered all the important aspects:

Gender roles in direct selling

Women in direct selling are moving ahead as one strong force as the business becomes a powerful platform for their empowering journey. According to the Global Entrepreneurship Monitor (GEM), there are more than 8 women starting new businesses for every 10 men doing the same.

With around 70% of direct sales representatives being women, the industry clearly has a strong female presence.

Source: WFDSA

Historically, women have dominated direct selling; however, an increasingly higher percentage of men are turning into this sector. This growing trend thus indicates a greater gender diversity within the industry.

Direct selling as a gateway for aspiring entrepreneurs

Direct selling is a source of flexible income, but the channel also offers a significant pathway to entrepreneurship for women. The GEM report points out that 1 in 6 women is planning to start a business soon, and direct selling often serves as their stepping stone into the entrepreneurial world. This way, women are able to build their own businesses while being supported by a community.

Key motivations for women entrepreneurs in direct selling

1. Job scarcity: As many as 73% of the female entrepreneurs cite the lack of job opportunities as their main motivation for starting a business.

2. Solopreneurs: 36% of these women operate as solopreneurs, that is, managing their ventures independently.

3. Wholesale and retail focus: Nearly 49% of female entrepreneurs in direct selling focus on wholesale and retail businesses. They capitalize on the direct selling infrastructure.

Age-wise categorization of representatives

Diversity and inclusivity form the hallmark of the modern-day direct selling. It is the age group of the distributors that plays a decisive factor in this case. This industry attracts a diverse range of age groups, and each one brings their distinct experience and perception to the table.

1. Young adults (18-34 years) 25.9% fall within the 34-and-under age group, pointing to opportunities for reaching younger demographics.

2. Prime age group (35-54 years) Nearly 49% of direct sellers fall within this age range. This demographic typically includes individuals in the mid-career stage.

3. Older representatives (54-above) 24.8% are above 54, which shows the industry's appeal to older individuals who seek flexible or additional income sources.

Strategic implications for the direct selling industry

To improve direct selling penetration, the industry needs well-thought-out strategies. Here are our insights and recommendations to guide the way forward.

1. Targeted marketing: Understanding the gender and age demographics allows direct selling companies to tailor their recruitment and marketing efforts more effectively.

2. Entrepreneurial support: Direct selling provides a valuable opportunity for women entrepreneurs. Companies can create programs to support their business development and help address job scarcity.

3. Diversity and inclusion: With more men and a wider age range among representatives, it’s essential to foster an inclusive environment that attracts a broad demographic spectrum.

What we’ve learned about direct selling's future

Direct selling has evolved into a significant global industry. It's interesting to see how it has established itself in different regions while appealing to a wide variety of consumers. The extensive WFDSA study highlights this growth with impressive data by clearly revealing that direct selling is expanding its footprint in established markets while making significant inroads into emerging economies. Behind the expansion lies a plethora of factors such as:

- Maturity assessment of the market

- Offering products that resonate with local consumers

- Increasing size and demographics of the salesforce

And so on (all that we’ve discussed already).

As direct selling continues to evolve along these MLM trends, the industry does bring forth new opportunities for entrepreneurs. Besides that, it’s also inspiring to see how the industry is committed to fostering inclusive and diverse business model. All in all, the future of direct selling looks truly promising. With innovation at the helm, the industry appears to respond to and meet the needs and expectations of the global market more effectively than ever before.

Leave your comment

Fill up and remark your valuable comment.